Understanding the Differences Between Personal and Business Credit Scores for Effective Financial Management

"Understanding the Differences Between Personal and Business Credit Scores for Effective Financial Management" dives into the key distinctions between personal and business credit scores, highlighting how each one influences your financial decisions and opportunities. This post explains the unique time frames, scoring systems, and financial responsibilities associated with each type of credit, offering insights on how to manage both effectively. Whether you're a business owner or an individual, this guide will help you navigate the credit landscape and optimize your credit profiles for better financial outcomes.

Gene and Laura Davis

8/9/202416 min read

Introduction to Credit Scores

Credit scores hold a critical role in personal and business financial management. Essentially, a credit score is a numerical representation of an individual's or business's creditworthiness as determined by credit agencies. These agencies evaluate various factors such as credit history, outstanding debts, and repayment behavior to calculate a score, which typically ranges from 300 to 850 for personal credit scores.

Understanding credit scores is important because they directly affect an individual's or business's ability to secure loans, credit cards, and favorable interest rates. For personal finances, a good credit score can streamline the process of obtaining mortgages, car loans, or even rental agreements. On the business side, a strong business credit score can facilitate access to financing, trade credit, and beneficial supplier terms. In this way, credit scores are pivotal in determining the financial opportunities available to both individuals and enterprises.

The importance of credit scores extends beyond just the ability to borrow money. They also influence insurance premiums, employment opportunities, and utility services, making them a comprehensive measure of financial reliability. Consequently, maintaining a good credit score should be a priority for effective financial management. Credit scores are derived from various scoring models, such as FICO and VantageScore, which assess the probability that a borrower will repay their debts based on past behavior and current credit status.

This introductory framework is crucial for diving deeper into the distinct aspects of personal and business credit scores, as each type has unique characteristics and implications. Subsequently, understanding the differences between these two categories can further enhance financial planning and management strategies, thereby optimizing both personal and corporate financial health.

Personal Credit Scores: A Detailed Overview

Personal credit scores serve as crucial indicators of an individual's creditworthiness. These scores range from 350 to 850 and are instrumental in determining loan approvals, interest rates, and even job prospects in some industries. Essentially, a personal credit score provides a snapshot of an individual's financial reliability over the previous 24-month period.

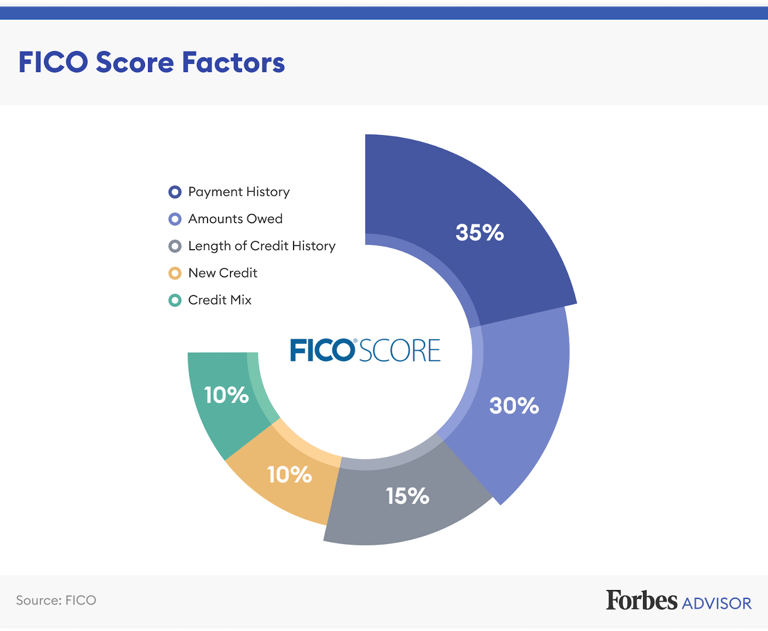

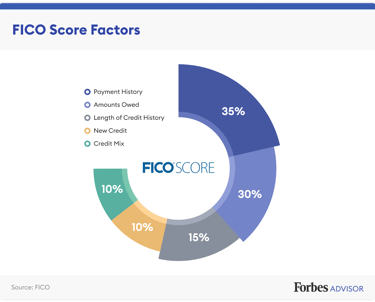

Several key factors contribute to the calculation of personal credit scores. First and foremost is payment history, accounting for approximately 35% of the score. Timely payment of bills and debts positively impacts this component, whereas late or missed payments can significantly lower the score. Another critical factor is credit utilization, which makes up about 30% of the score. This is the ratio of current debt to available credit, with lower ratios typically being more favorable.

The length of credit history, which contributes around 15%, looks at the age of an individual's oldest account and the average age of all accounts. A longer credit history often indicates responsible credit management. New credit, encompassing about 10% of the score, considers recent credit inquiries and newly opened accounts. Multiple inquiries or numerous newly opened accounts in a short time can negatively affect the score.

Lastly, credit mix, making up the final 10%, examines the variety of credit accounts held, such as credit cards, mortgages, and auto loans. A diverse credit portfolio is generally viewed positively as it demonstrates the ability to manage different types of credit effectively.

Personal financial behaviors greatly influence these factors. For instance, paying off balances on time, maintaining low balances relative to credit limits, and avoiding opening numerous accounts simultaneously can help in maintaining or improving a personal credit score. Regularly monitoring one's credit report for inaccuracies can also mitigate potential drops in the score.

Through an understanding of personal credit scores and the behaviors that impact them, individuals can take meaningful steps toward effective financial management and better credit health.

Business Credit Scores: Essential Insights

Business credit scores are crucial for assessing a company's creditworthiness and overall financial health. These scores typically range from 0 to 100 and gauge the likelihood of a company defaulting on financial obligations within a 12-month period. Understanding the factors influencing these scores can help businesses maintain robust financial standings and gain access to better financial opportunities.

Several key factors impact business credit scores. Firstly, a company’s financial obligations, including any outstanding loans or lines of credit, play a significant role. Timely repayment of these obligations positively affects the credit score, demonstrating financial reliability. Secondly, payment history is pivotal; consistent on-time payments are essential to maintaining a high credit score. Conversely, late payments can significantly lower the score.

Credit utilization, which refers to the ratio of used credit to the total available credit, is another crucial factor. Keeping credit utilization low suggests prudent financial management and can enhance credit ratings. Additionally, the size and age of the business are also relevant. Established companies often have higher scores due to extensive credit histories, while larger businesses may be perceived as more stable, positively influencing their scores.

Examples of business financial behavior impacting credit scores illustrate these points clearly. For instance, a business that regularly meets its debt obligations and maintains low credit utilization will likely see an improvement in its credit score. On the other hand, a company with frequent late payments or high outstanding debt may face lower scores, adversely affecting its capacity to secure financing.

To maintain or enhance a business credit score, timely payments and responsible credit use are fundamental. Regularly monitoring the credit report for any discrepancies and actively managing debts can prevent adverse impacts. Establishing strong financial practices and maintaining a balance between credit used and available credit is essential for sustaining a positive business credit score, ultimately paving the way for better financial management and growth opportunities.

Key Differences Between Personal and Business Credit Scores

In distinguishing personal and business credit scores, it is paramount to understand that they serve different purposes and are evaluated on separate criteria. Personal credit scores typically span from 350 to 850, reflecting an individual's creditworthiness based on consumer debt, personal loans, and credit cards. In contrast, business credit scores range from 0 to 100, focusing solely on the creditworthiness of a business entity, considering its invoices, trade credits, and business-specific financial obligations.

The evaluation period also differs significantly between the two. Personal credit scores consider a longer period of financial behavior, often up to 24 months. This extended duration allows for a more nuanced view of an individual's credit habits, capturing any long-term trends in financial responsibility. On the other hand, business credit scores are often reviewed within a shorter window of 12 months. This condensed timeframe aims to provide a real-time assessment of a business's current financial health, acknowledging the dynamic nature of business operations and financial commitments.

The factors influencing these scores also vary. Personal credit scores are influenced by payment history, credit utilization, length of credit history, new credit inquiries, and types of credit used. Meanwhile, business credit scores are heavily reliant on trade credit experiences, payment trends, the financial stability of the business, and public records such as bankruptcies and liens. These differentiated factors highlight the unique dynamics in financial management for individuals versus businesses.

For example, timely personal credit payments can enhance access to better mortgage rates, whereas consistent business payment records can improve credit terms with suppliers, impacting cash flow management. Further, while a high personal credit score can lead to lower interest rates on personal loans, a robust business credit score can facilitate larger credit arrangements, necessary for expansion and growth.

Understanding these key differences between personal and business credit scores is essential for tailored financial management strategies. Both individuals and business owners must recognize these distinctions to optimize their financial decision-making processes effectively.

Maintaining Separation Between Personal and Business Finances

Maintaining a clear separation between personal and business finances is crucial for accurate credit scoring and effective financial management. This fundamental practice starts with the establishment of distinct bank accounts for personal and business transactions. By opening separate checking accounts, transactions remain categorized, preventing the commingling of funds, which can lead to confusion and potential issues during financial assessments.

Furthermore, the use of different credit cards for personal and business purposes significantly augments this separation. Business credit cards often offer specific features and benefits tailored to business needs, such as expense tracking and business-specific rewards. By consistently using a business credit card for all business-related expenditures, the financial delineation becomes more pronounced, streamlining bookkeeping processes and providing a clearer picture of business financial health. Moreover, this practice positively impacts credit management, as it ensures business credit histories are built independently of personal credit, consequently aiding in improved credit scoring for both realms.

Proper documentation and meticulous record-keeping are also vital strategies to maintain financial separation. Utilizing accounting software that distinctly categorizes personal and business expenses can greatly enhance organization. Keeping receipts, invoices, and financial statements systematically filed not only simplifies the preparation for tax filings but also aids in providing clear evidence of transactions in case of audits. Adopting these practices helps small business owners avoid the pitfalls of blended finances, leading to better financial visibility and decision-making.

The benefits of maintaining a separation between personal and business finances extend beyond organizational efficiency. It simplifies tax filings by providing clear distinctions between deductible business expenses and personal expenditures, thus avoiding potential tax complications. In addition, it enhances credit management by reflecting a more accurate credit profile for each respective area, leading to opportunities for favorable credit terms and better financial growth. Through diligent adherence to these strategies, business owners can attain more effective financial management and ensure the robustness of their financial standing.

Monitoring and Leveraging Credit Scores for Growth

Regular monitoring and strategic leveraging of your credit scores are essential components of effective financial management. Tracking both personal and business credit scores can provide insights necessary for informed decision-making and can help in securing advantageous financing options. One of the most efficient ways to track credit scores is by utilizing credit monitoring services. These services provide real-time alerts and comprehensive reports, allowing individuals and businesses to stay updated on their credit status and identify any unusual activity promptly.

In addition to relying on these services, regularly reviewing credit reports from major credit bureaus is recommended. This practice ensures that all the information reported is accurate and up-to-date. If discrepancies are found, it is crucial to address them immediately by contacting the credit bureau and providing necessary documentation to correct the errors. Timely resolution of such issues can prevent potential negative impacts on your credit score.

Leveraging strong credit scores can open doors to numerous financial opportunities. For businesses, a high credit score can lead to better interest rates on loans, increased credit limits, and more favorable terms with suppliers. These advantages can translate to enhanced cash flow and greater investment capabilities, driving business growth. Similarly, individuals with robust personal credit scores may find themselves eligible for low-interest personal loans, premium credit cards, and mortgage options that align with their financial goals.

Practical tips for improving credit scores include maintaining low credit card balances, refraining from closing old accounts, and ensuring timely payments of bills and outstanding debts. Diversifying credit types and minimizing the number of hard inquiries can also contribute positively to your credit profile. Both personal and business credit improvement require consistent effort, but the rewards, in terms of financial flexibility and growth opportunities, are substantial.

By keenly monitoring and strategically leveraging credit scores, individuals and businesses can navigate the financial landscape more effectively, unlocking potential avenues for growth and stability.

Understanding the differences between personal and business credit scores is crucial for both individuals and business owners. While both types of scores evaluate creditworthiness, they do so in distinct ways, reflecting different aspects of financial behavior and risk.

In today's financial landscape, understanding the distinctions between personal and business credit scores is more important than ever. Whether you're an individual looking to secure a mortgage or a business owner seeking a line of credit, knowing how these scores operate and affect your financial opportunities can make all the difference in the world!

While both personal and business credit scores evaluate creditworthiness, they do so in ways that reflect different aspects of financial behavior and risk. In this post, we will delve into three significant differences between personal and business credit scores, highlighting their implications and providing insights into effectively managing both.

Here are three significant differences between personal and business credit scores:

3 Big Differences Between Personal Credit Scores and Business Credit Scores

1. Time Frame for Risk Assessment

One of the most fundamental differences between consumer and business credit scores is the time frame over which they assess the risk of default. This distinction impacts how quickly your credit score can change and the frequency with which you should monitor it.

Business Credit Scores: A Shorter Time Frame

Business credit scores are designed to assess a business's risk of going 90 days late on an account within the next 12 months. This shorter time frame means that business credit scores are more dynamic and can change more rapidly based on recent payment behaviors and financial activities. For business owners, this necessitates a proactive approach to credit management. Even a slight delay in payment or an unexpected financial hiccup can lead to a noticeable change in your business credit score.

Because of the shorter assessment period, business credit scores require more frequent monitoring. If a business fails to stay on top of its financial obligations, its credit score can quickly reflect this, making it harder to secure favorable terms on loans, credit lines, or supplier agreements. The dynamic nature of business credit scores makes them both a powerful tool for growth and a potential vulnerability if not managed carefully.

Personal Credit Scores: A Broader View

In contrast, personal credit scores evaluate a consumer’s risk of going 90 days late on an account within the next 24 months. This extended time frame means that personal credit scores take a broader view of your credit history, considering a more extended period of financial behavior. As a result, personal credit scores are typically less volatile than business credit scores.

While this longer assessment period offers some cushioning against the impact of short-term financial issues, it also means that improving a personal credit score can take more time. Positive financial behaviors, such as paying off debts or reducing credit utilization, may take longer to reflect in your score, but they contribute to a more stable and reliable credit profile in the long run.

Implication: The Need for Frequent Monitoring in Business Credit

The key takeaway here is that business credit scores require more frequent monitoring and proactive management to maintain a good score, as recent activities have a more immediate impact. On the other hand, personal credit scores offer a more stable reflection of your creditworthiness but require consistent long-term financial discipline.

2. What the Score Represents

Another major difference between personal and business credit scores lies in what the score represents and whom it reflects. This distinction is crucial for maintaining separate financial identities for personal and business endeavors.

Consumer Credit Scores: A Measure of Personal Financial Behavior

Consumer credit scores, such as those generated by FICO or VantageScore, reflect an individual’s likelihood of defaulting on an obligation. These scores are a measure of your creditworthiness based on personal financial behaviors, including payment history, debt levels, credit mix, and more. Lenders use these scores to assess your risk as a borrower when considering applications for personal loans, mortgages, credit cards, and other financial products.

Because personal credit scores are tied directly to your social security number and personal financial activities, they paint a comprehensive picture of your individual credit habits. A high personal credit score indicates that you manage your personal finances responsibly, making you a lower risk for lenders.

Business Credit Scores: Reflecting the Business's Financial Health

In contrast, business credit scores reflect the business's likelihood of defaulting on an obligation, independent of the business owner's personal credit behaviors. These scores are derived from how the business meets its financial obligations, including payments to suppliers, lenders, and other creditors. Business credit scores are tied to the business’s Employer Identification Number (EIN) and are separate from the owner’s social security number.

This separation allows for a clearer distinction between personal and business financial responsibilities. A business with a strong credit score can secure financing, negotiate better terms with suppliers, and expand its operations without directly affecting the owner's personal credit. Conversely, a business with poor credit might struggle to grow or even maintain its operations, regardless of the owner's personal creditworthiness.

Implication: The Importance of Maintaining Separate Financial Identities

The implication here is that maintaining a strong business credit score provides a separate financial identity for the business, which is crucial for both protecting the owner's personal credit and ensuring the business's ability to thrive. Business owners should be diligent in managing their business credit, just as they would with their personal credit, to ensure that their business remains financially healthy and capable of growth.

Consumer Credit Scores: The Familiar 350-850 Range

Typically, personal credit scores, such as FICO scores, range from 350 to 850. In this range, an 850 score is considered the highest and best possible, indicating exceptional creditworthiness. Personal credit scores are calculated based on a variety of factors, including payment history, amounts owed, length of credit history, new credit, and credit mix. Each of these factors contributes to the overall score, with payment history and amounts owed being the most significant.

Most consumers are familiar with the 350-850 range, and many financial products, such as loans and credit cards, come with specific credit score requirements within this range. A score above 700 is generally considered good, while a score above 800 is excellent.

Business Credit Scores: A More Condensed 0-100 Scale

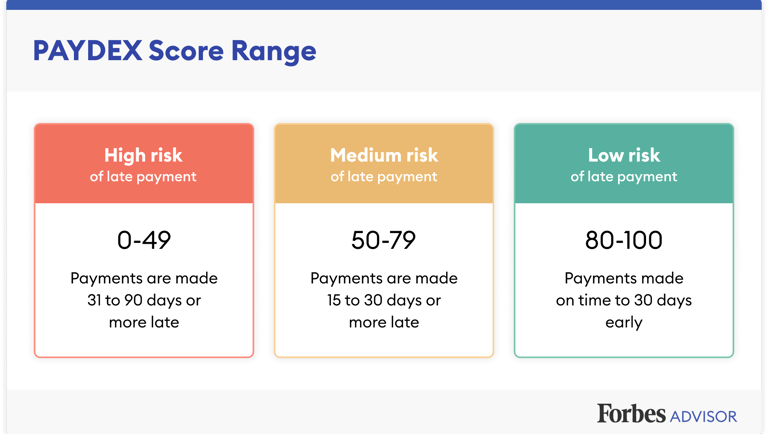

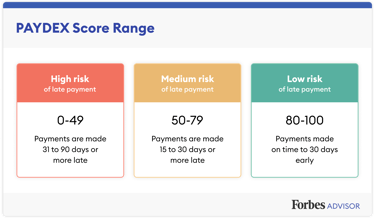

Business credit scores, on the other hand, often range from 0 to 100, with 100 being the top score. Different business credit bureaus might use slightly varied ranges or models, but the 0-100 scale is common. For example, Dun & Bradstreet's PAYDEX score, one of the most well-known business credit scores, operates on a 0-100 scale, with scores of 80 or above considered very good.

This more condensed range reflects the nature of business credit evaluation, where the primary focus is on payment behavior. A business that consistently pays its bills on time or early will likely have a high score, while late payments can quickly drag the score down.

Implication: Understanding and Interpreting Different Scales

The key implication here is that the scoring scales for personal and business credit are not directly comparable, and the interpretation of what constitutes a good score differs between the two. For business scores, a score of 80 or above is generally considered very good, indicating a low risk of late payments. Business owners should familiarize themselves with the specific scoring model used by the business credit bureaus they interact with to understand what constitutes a good score in their particular context.

3. Score Range

The range within which personal and business credit scores fall is another significant difference. This difference in scoring scales reflects the distinct methods and criteria used to evaluate creditworthiness in personal and business contexts.

Consumer Credit Scores: The Familiar 350-850 Range

Typically, personal credit scores, such as FICO scores, range from 350 to 850. In this range, an 850 score is considered the highest and best possible, indicating exceptional creditworthiness. Personal credit scores are calculated based on a variety of factors, including payment history, amounts owed, length of credit history, new credit, and credit mix. Each of these factors contributes to the overall score, with payment history and amounts owed being the most significant.

Most consumers are familiar with the 350-850 range, and many financial products, such as loans and credit cards, come with specific credit score requirements within this range. A score above 700 is generally considered good, while a score above 800 is excellent.

Business Credit Scores: A More Condensed 0-100 Scale

Business credit scores, on the other hand, often range from 0 to 100, with 100 being the top score. Different business credit bureaus might use slightly varied ranges or models, but the 0-100 scale is common. For example, Dun & Bradstreet's PAYDEX score, one of the most well-known business credit scores, operates on a 0-100 scale, with scores of 80 or above considered very good.

This more condensed range reflects the nature of business credit evaluation, where the primary focus is on payment behavior. A business that consistently pays its bills on time or early will likely have a high score, while late payments can quickly drag the score down.

Implication: Understanding and Interpreting Different Scales

The key implication here is that the scoring scales for personal and business credit are not directly comparable, and the interpretation of what constitutes a good score differs between the two. For business scores, a score of 80 or above is generally considered very good, indicating a low risk of late payments. Business owners should familiarize themselves with the specific scoring model used by the business credit bureaus they interact with to understand what constitutes a good score in their particular context.

Additional Differences and Considerations

Beyond these three primary differences, there are several other aspects to consider when comparing personal and business credit scores. These additional factors can significantly impact how credit is managed and utilized in both personal and business settings.

Reporting Agencies

One key difference lies in the agencies that report and track credit scores. Personal credit is typically reported to three major bureaus—Equifax, Experian, and TransUnion. These agencies collect information about your credit accounts, payment history, and public records to generate your credit score.

Business credit, however, is reported to agencies such as Dun & Bradstreet, Experian Business, and Equifax Business. Each of these agencies may use different methods and criteria to evaluate business credit, and not all lenders or suppliers report to all business credit bureaus. As a result, business owners need to monitor their credit reports across multiple agencies to get a complete picture of their business credit profile.

Factors Influencing Scores

The factors that influence personal and business credit scores also differ. Personal credit scores are influenced by payment history, amounts owed, length of credit history, new credit, and credit mix. Each of these factors contributes to the overall score, with payment history and amounts owed being the most significant.

Business credit scores, on the other hand, are primarily influenced by payment history, the age of credit lines, debt usage, and company size. Payment history is the most critical factor, as timely payments to suppliers, lenders, and creditors are essential for maintaining a strong business credit score. Additionally, the size of the company and the age of its credit lines can impact the score, with older, more established businesses typically having higher scores.

Impact of Scores

The impact of personal and business credit scores extends beyond simply securing loans or credit lines. Personal credit scores impact your ability to get personal loans, mortgages, credit cards, and even affect things like insurance premiums and rental applications. A poor personal credit score can limit your financial opportunities and increase the cost of borrowing.

Business credit scores, however, affect a business's ability to secure loans, lines of credit, and favorable terms with suppliers. A strong business credit score can help a business secure financing with lower interest rates, negotiate better payment terms with suppliers, and even attract potential investors. Conversely, a poor business credit score can make it difficult for a business to grow and expand, as it may struggle to secure the necessary funding or favorable terms.

Conclusion: The Importance of Understanding Credit Scores

Understanding the differences between personal and business credit scores is essential for effectively managing both personal and business finances. By recognizing the distinct time frames, representations, and scoring ranges, you can better navigate the credit landscape and leverage each type of credit to your advantage.

Key Takeaways

Monitor Regularly: Given the shorter assessment period for business credit, frequent monitoring and proactive management are crucial.

Maintain Separation: Keep personal and business finances separate to protect your personal credit score and ensure your business credit score reflects your business’s financial health.

Understand Scales: Familiarize yourself with the different scoring scales and what they represent, so you can accurately assess your creditworthiness in both personal and business contexts.

By staying informed and proactive, you can build strong personal and business credit profiles that open doors to financial opportunities and success. By understanding these differences, you can better manage your credit profiles and ensure you’re well-positioned to secure the financing needed for personal and business growth

Let's talk

customersupport@eincreditfunding.com

888-599-1830 ext 702